Introduction

Buying a vehicle doesn’t have to involve lengthy bank applications or complicated paperwork. Inhouse vehicle finance offers a faster and more convenient way to purchase a car by allowing the dealership to handle the financing directly. Whether you have excellent credit, bad credit, or no credit history, in-house financing can provide flexible solutions that help you drive away sooner.

Inhouse vehicle finance refers to the process of financing a vehicle whereby the dealer takes the role of the financier rather than using banks or other financial institutions. The buyers are able to apply for the loan, get approved, and buy the car at one single location.

What Is Inhouse Vehicle Finance?

Inhouse vehicle finance refers to the process of financing a vehicle whereby the dealer takes the role of the financier rather than using banks or other financial institutions. The buyers are able to apply for the loan, get approved, and buy the car at one single location.The dealers that offer in-house financing tend to focus more on buyers who have previously been denied financing due to bad credit ratings among others.

Benefits of Inhouse Vehicle Finance

1. Fast Approval Process

One of the biggest advantages of in-house vehicle finance 1is the quick approval process. Since dealerships make lending decisions internally, approvals are often completed within hours rather than days.

Flexible Payment Plans

Dealerships can customize payment schedules based on your financial situation. Many offer:

- Weekly payments

- Bi-weekly installments

- Monthly payment options

- Adjustable loan terms

This flexibility makes budgeting easier for many buyers. Unlike traditional lenders, dealerships often consider factors beyond your credit score, including:

- Current income

- Employment stability

- Down payment amount

- Ability to repay

This makes in-house vehicle finance an attractive option for individuals with:

- Bad credit

- No credit history

- Previous bankruptcies

- Self-employment income

Convenient One-Stop Financing

Everything happens at the dealership:

- Choose your vehicle

- Apply for financing

- Receive approval

- Sign paperwork

- Drive home

This streamlined process saves time and reduces stress.

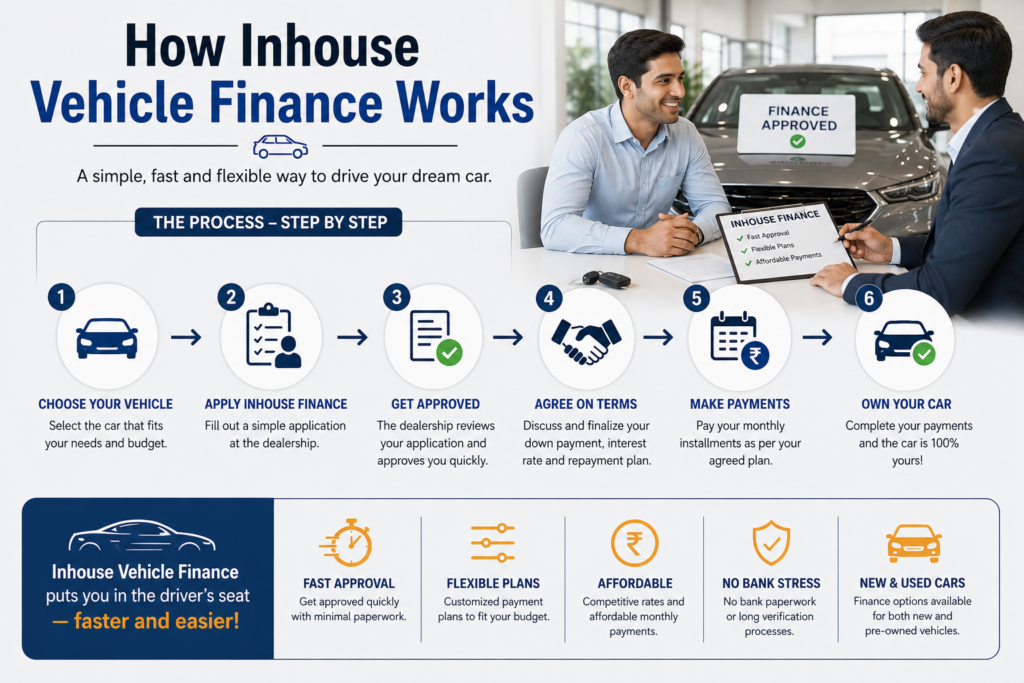

How Inhouse Vehicle Finance Works

The process is typically straightforward:

- Select the vehicle you want.

- Complete a finance application.

- Provide proof of income and identification.

- Receive a financing decision.

- Review your payment plan.

- Finalize the agreement and take delivery of your vehicle.

Many dealerships can complete the entire process on the same day.

Who Should Consider Inhouse Vehicle Finance?

In-house vehicle finance is ideal for:

- First-time car buyers

- Buyers with poor credit

- Individuals rebuilding credit

- Self-employed workers

- Customers needing fast vehicle approval

- People without extensive credit history

Tips for Getting Approved

To improve your chances of approval:

- Bring proof of stable income.

- Save for a larger down payment.

- Have valid identification and proof of residence.

- Be honest about your financial situation.

- Choose a vehicle that fits your budget.

These steps can increase approval odds and may help secure better loan terms.

Understanding Interest Rates

Interest rates for in-house vehicle finance can vary depending on:

- Credit history

- Loan amount

- Vehicle age

- Down payment

- Loan term

While rates may be higher than traditional bank financing, many borrowers value the easier approval process and opportunity to rebuild their credit through consistent, on-time payments.

Can Inhouse Vehicle Finance Help Build Credit?

Many dealerships report payment activity to major credit bureaus. Making timely payments may help improve your credit profile over time. Before signing your agreement, ask whether the dealership reports payments to credit reporting agencies.

Things to Consider Before Signing

Before accepting an in-house vehicle finance agreement, carefully review:

- Interest rate (APR)

- Total loan cost

- Payment schedule

- Late payment penalties

- Early repayment options

- Warranty coverage

- Vehicle condition

Understanding these details helps you avoid unexpected costs later.

Why Buyers Choose Inhouse Vehicle Finance

Many drivers choose in-house vehicle finance because it offers:

- Fast approvals

- Flexible payment plans

- Simplified application process

- Less emphasis on credit scores

- Convenient dealership financing

- Opportunities for credit rebuilding

For buyers who need reliable transportation without the hurdles of traditional bank loans, in-house financing can be a practical and accessible solution.

Final Thoughts

How Can Inhouse Vehicle Finance Help Build Credit?

Most dealerships report their customer payments to big credit bureaus. It may help to build a positive credit history. Before signing the contract, find out if the dealer reports your payments to credit bureaus. Points to Consider Before Signing the Agreement

When considering taking an in-house vehicle financing agreement, make sure you understand the following information:

- Interest Rate (APR)

- Loan cost total

- Repayment terms

- Late payment fees

- Possibilities of early repayment

- The warranty

- Condition of the vehicle

All these points will help you to avoid unnecessary expenses. Why Drivers Prefer Inhouse Vehicle Finance

There are some reasons why many buyers prefer in-house vehicle finance:

- Quick Approvals

- Flexible Repayment Plans

- Easy Application Process

- Minimal focus on credit score

- Convenient Financing at a Dealership

- Credit Rebuilding Possibilities

Drivers who need to have a reliable vehicle but cannot go through the trouble of applying for a traditional bank loan may use this financing method.

Conclusion

Inhouse vehicle finance is a convenient way to purchase a car quickly, with flexible payment options, and easy access to financing services.

Before committing, compare financing offers, understand the loan terms, and ensure the monthly payments comfortably fit your budget. Making informed decisions today can help you enjoy affordable vehicle ownership while strengthening your financial future “To understand more about auto loan options, you can check the offical Consumer Financial Protection Bureau guidelines.